How insurers can harness untapped multi-billion naira pension en bloc business via immediate annuity

Kindly leave a comment and share

Chuks Udo Okonta

If well positioned life insurance companies through immediate annuity product can harness the untapped multi-billion naira pension en bloc business which the National Pension Commission (PenCom) said a total of ₦14.15 billion was approved for disbursement in the first quarter 2025 to retirees whose Retirement Savings Account (RSA) balances cannot support a monthly pension of at least one-third of the ₦70,000 minimum wage.

According to PenCom in Q1 2025, 11,809 retirees were approved to access their pensions through en bloc payments, a provision for those whose RSA balances cannot support a

monthly pension of at least one-third of the ₦70,000 minimum wage, this means that the retirees are now without a pension benefits payment package.

Though their en bloc payment may seem small, but if the retirees are properly educated by insurance operators, they can beef up the fund with any other available funds to procure immediate annuity that would enable them to have a monthly pension benefits payment scheme.

PenCom stated that the private sector accounted for the majority of approvals, with 10,423 retirees 88.3 per cent, underscoring its higher proportion of low-balance RSA holders. In

contrast, only 1,400 approvals 11.7 per cent came from the public sector, reflecting

generally stronger RSA balances.

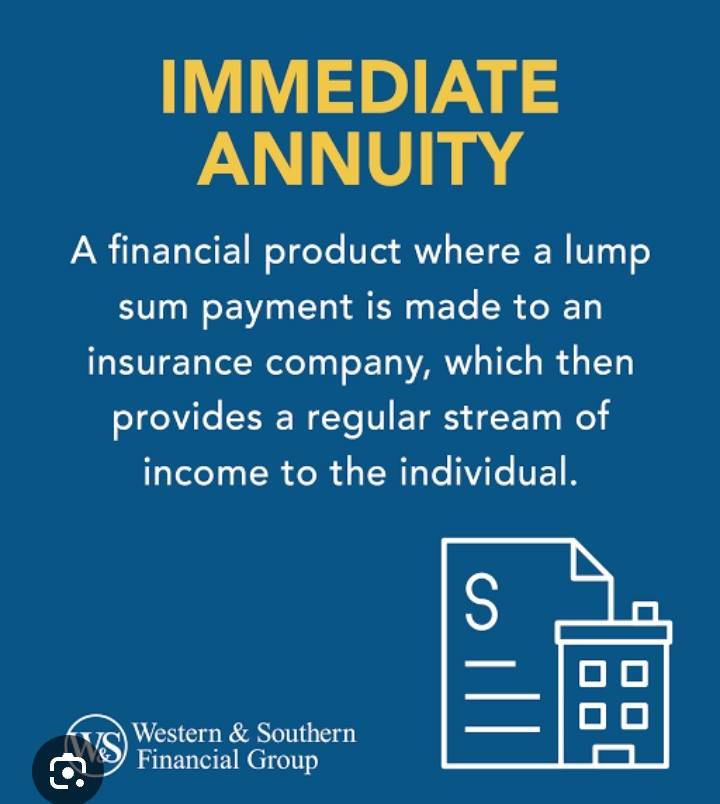

An immediate annuity, also known as a Single Premium Immediate Annuity (SPIA), is an insurance contract that converts a single, lump-sum payment into a guaranteed stream of regular income, typically starting within one month to one year of purchase.

It is primarily used by retirees who want to ensure a stable, predictable income stream to cover their living expenses.

How It Works

Single Premium:

You purchase the annuity from an insurance company with one large sum of money (premium). This money often comes from existing retirement savings like en bloc, lump sum, addition voluntary contribution amongst others.

Immediate Payouts:

Unlike deferred annuities which have a growth (accumulation) phase, immediate annuities start paying you back almost right away.

Guaranteed Income:

In exchange for your premium, the insurance company contractually guarantees you regular payments for a chosen length of time, such as a set number of years or the rest of your life (and potentially a beneficiary’s life).

No Accumulation Phase:

There is no period for the money to grow tax-deferred within the annuity before payments begin.